DEVON ENERGY CORP/DE (DVN)·Q4 2025 Earnings Summary

Devon Energy Beats Q4 Estimates, Announces Transformational Coterra Merger

February 17, 2026 · by Fintool AI Agent

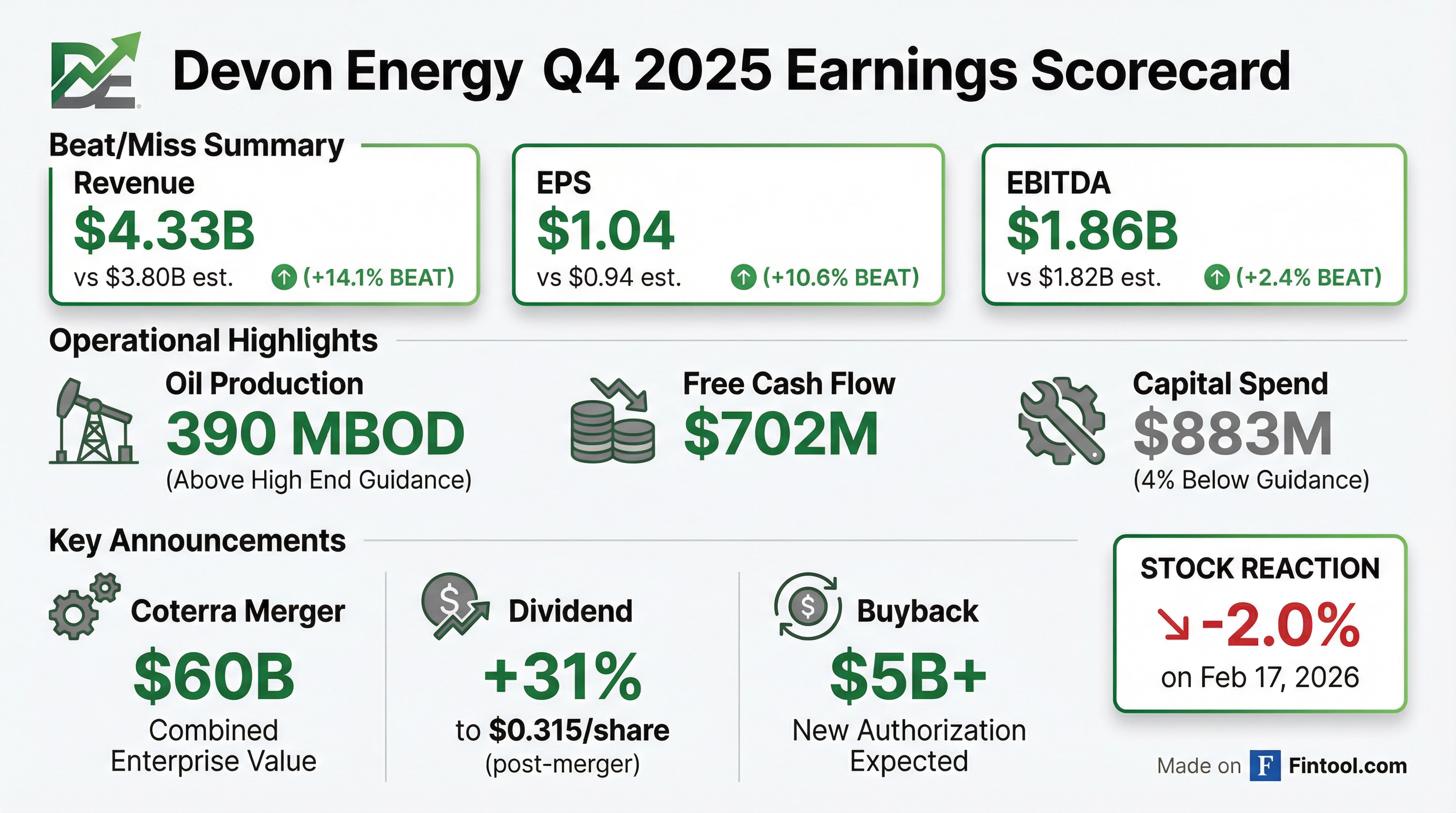

Devon Energy delivered a strong Q4 2025, beating consensus estimates across all key metrics while unveiling a transformational merger with Coterra Energy that will create one of the largest independent shale operators in the U.S. with a ~$60 billion pro forma enterprise value.

The quarter showcased Devon's operational excellence with oil production of 390,000 barrels per day exceeding the high end of guidance, while capital spending came in 4% below midpoint at $883 million. The company generated $702 million of free cash flow and returned approximately $400 million to shareholders through dividends and buybacks.

Did Devon Beat Earnings?

Yes — Devon beat on all three key metrics:

Values retrieved from S&P Global

Devon reported GAAP net earnings of $562 million, or $0.90 per diluted share. Core earnings (excluding one-time items) were $510 million, or $0.82 per diluted share. Operating cash flow totaled $1.5 billion for the quarter.

What Drove the Beat?

Production Outperformance

Total production averaged 851,000 Boe per day, exceeding the top end of guidance. Oil production of 390,000 barrels per day was particularly strong, representing 46% of total volumes.

Production by Basin (Q4 2025):

Capital Discipline

Capital investment of $883 million came in 4% below guidance midpoint, driven by effective cost management and timing of facility spending. Full-year 2025 capital spending of $3.64 billion represented a $460 million improvement since late 2024.

Operating Cost Improvements

Production costs (LOE + GP&T) declined to $8.60 per BOE in Q4, an 8% reduction from Q1 2025. This improvement reflects Devon's business optimization initiatives and effective cost management.

What Is the Coterra Merger?

On February 2, 2026, Devon announced an all-stock merger with Coterra Energy that will create a premier large-cap shale operator.

Key Merger Terms:

The combination creates an undisputed Delaware Basin leader with over 10 years of highly competitive drilling inventory. The Delaware Basin will underpin over 50% of enterprise-wide production and free cash flow.

CEO Clay Gaspar stated: "This powerful combination brings together two industry-leading companies with complementary assets and proven track records of value creation, establishing a premier independent shale operator."

What Did Management Guide?

Q1 2026 Outlook (Standalone Devon)

Note: Q1 production includes an estimated 1% reduction (~10,000 Boe/d) due to severe winter weather impact.

Full-Year 2026 Outlook (Standalone)

Updated full-year guidance for the combined entity will be provided following merger close.

What About Shareholder Returns?

Devon announced significant enhancements to its capital return program following merger close:

Dividend:

- Current quarterly dividend: $0.24 per share

- Planned post-merger dividend: $0.315 per share (+31% increase)

- Subject to board approval following merger close

Share Buybacks:

- 2025 repurchases: $1.05 billion

- Shares retired: ~14% of outstanding since program inception

- New authorization expected: >$5 billion post-merger

- Current buyback activity suspended through merger close

2025 Total Shareholder Returns:

- Share buybacks: $1.05 billion

- Dividends paid: $619 million

- Debt retirement: $485 million

- Total: ~$2.2 billion

What Changed From Last Quarter?

The sequential decline in free cash flow reflects lower commodity prices in Q4 (WTI averaged $59.09 vs $64.92 in Q3).

Business Optimization Progress

Devon achieved 85% of its $1 billion business optimization target as of Q4 2025 exit rate, ahead of schedule. The company remains on track to fully achieve the target by year-end 2026.

Key Optimization Drivers:

- Capital Efficiency: 9% faster drilling, 21% faster completions YoY

- Production Optimization: Q4 exit-rate delivered 36 MBOED uplift from original guidance

- Commercial Opportunities: $200M in annual Delaware Basin contract savings

- Corporate Costs: $485M notes retired in Sept 2025, $1B term loan repayment planned Q3 2026

How Did the Stock React?

Devon shares closed at $44.06 on February 17, 2026, down 2.0% on the day.

Stock Performance:

Data from market-data skill

The modest pullback on earnings day came despite the strong operational results, likely reflecting investor digestion of the Coterra merger terms and broader energy sector dynamics.

Balance Sheet & Liquidity

Devon ended Q4 with a strong financial position:

Pro forma for the Coterra merger, the combined company will have 0.9x net debt-to-EBITDAX and $4.5 billion of liquidity.

Additional Value Creation in 2025

Devon delivered over $1 billion in value uplift through proactive asset management in 2025:

- Eagle Ford JV Dissolution: $2.7M per well D&C savings, gained operatorship flexibility

- Cotton Draw Midstream Acquisition: $260M for non-controlling interest, ~$50M annual distribution savings

- Matterhorn Pipeline Divestiture: Sold equity interest for $409M

- WaterBridge IPO: 14% ownership valued at ~$400M

- Fervo Energy Investment: ~15% ownership stake following Series E funding round

Key Risks & Considerations

- Merger Execution Risk: The Coterra transaction is subject to shareholder and regulatory approvals with expected Q2 2026 close

- Commodity Price Exposure: Q4 realized prices declined vs Q3 (WTI $59.09 vs $64.92)

- Winter Weather Impact: Q1 2026 production expected to be reduced by ~1% due to severe weather

- Integration Challenges: Achieving $1B synergies by 2027 requires successful integration

Forward Catalysts

Related Links: